Every consultant who works near money eventually meets the Standby Letter of Credit pitch, the classic SBLC scam dressed up as ordinary trade finance. It arrives dressed for the occasion: a real industry, a plausible deal, the name of a genuine bank, and an offer that sounds like ordinary trade finance. The version described in this article came through a consulting enquiry from a newly-formed Dubai gold-trading company, call it Meridian Metals, a stand-in name, since the specifics of the firm are not the point. The pattern is the point, because it repeats across continents and decades with almost no variation.

What follows is the full anatomy: how the instrument actually works, how the scam imitates it, why a real bank in the chain proves nothing, the three ways these stories end, the documented criminal cases that match the script almost word for word, and the verification steps that collapse the whole thing in forty-eight hours. None of it requires being a lawyer. Most of it requires only refusing to skip steps.

- The setup

- What an SBLC actually is

- How the SBLC scam imitates the real thing

- The three ways it ends

- The regulators have said this out loud

- The red-flag checklist

- What to use instead

- The first twist: who is the beneficiary?

- The second twist: the “fund,” and a real bank as set dressing

- The documented cases that match the script

- United States v. Douglas, Mignott, Gillar (D.N.J., 24 October 2022)

- United States v. Markowitz & Binet (S.D.N.Y., 6 March 2020)

- United States v. Hampton, Kuzma, Davis (D.N.J., 1 June 2022)

- The economics don’t close

- The verification sequence

- The broader pattern: gold, Dubai, and trade-based laundering

- The lesson, compressed

- Frequently asked questions

- Can you “lease” or “rent” an SBLC from a third party?

- What is the real cost of an SBLC?

- Is an MT799 message proof that an SBLC has been issued?

- How can I verify if an SBLC offer is legitimate?

- Need a second opinion on a deal?

- Related trade finance guides

- Need a consultation?

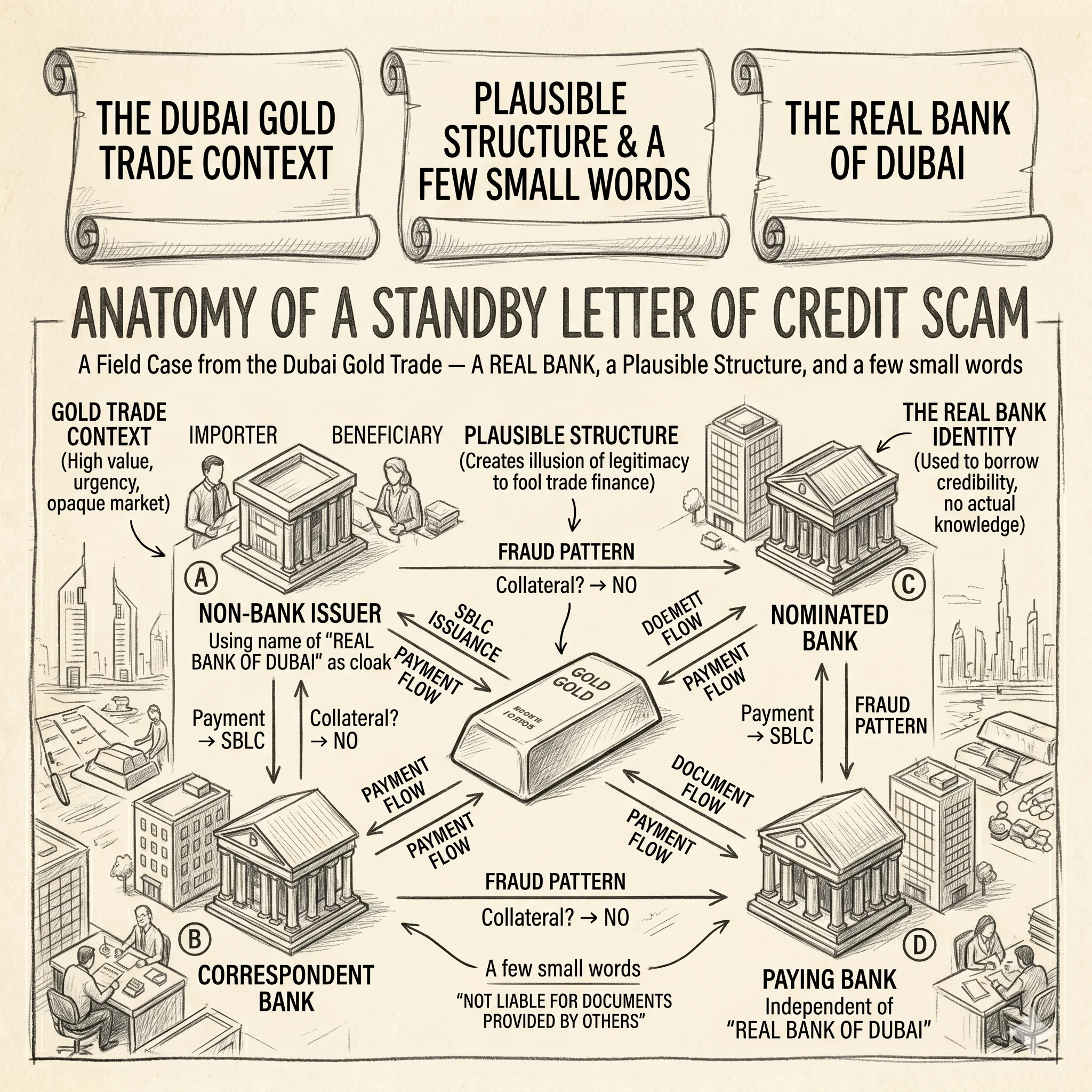

The setup

Meridian imports gold from Africa into the UAE. Their suppliers, as suppliers in this trade frequently do, asked for a Standby Letter of Credit (SBLC) as a guarantee of payment. Meridian found, as everyone eventually does, that “there is a market” of intermediaries offering help arranging the instrument. The specific offer: an SBLC issued by a bank in another jurisdiction, arranged by a third party, without Meridian opening an account at that bank. The fee floated around 3–4%, payable, they were told, only after the beneficiary’s bank confirmed receipt of the SBLC.

Their question, to their credit, was the right one: is this a legitimate instrument, or is this an SBLC scam?

The honest first answer is that the phrase “issued by a third-party bank, in another jurisdiction, without opening an account there” describes one of the most documented fraud structures in the history of trade finance, the textbook SBLC scam. It travels under several names, leased SBLC, rented bank instrument, non-account SBLC. The label changes; the mechanics don’t.

What an SBLC actually is

An SBLC is a bank guarantee. In plain terms: a bank promises to pay your supplier in your place if you fail to perform your side of the contract. It is insurance for the beneficiary, not a source of cash for the applicant.

For a bank to issue such a guarantee, the applicant must have an account there with funds blocked as full collateral, cash, eligible securities, or an approved credit line, and must sign a counter-indemnity, a binding promise to reimburse the bank for any payment it makes under the guarantee. There is no path around this. A bank cannot issue a guarantee for a non-customer because it has nowhere to lock collateral and no one to pursue for reimbursement if it has to pay. This is not “the bank is reluctant”; it is “the bank physically cannot.”

The guarantee itself moves through the secure interbank network, SWIFT, as a message in the MT760 format, sent bank-to-bank between the issuer and the beneficiary’s bank. A PDF, a photograph, a “swift copy” screenshot, none of these is a guarantee. The MT799 message, which fraudsters love to wave around as “proof,” is a free-format advisory note. Legally it is nothing.

The whole instrument is governed by the International Chamber of Commerce rules, ISP98 and UCP 600. Anything that lives outside those rules is, by definition, not an SBLC.

How the SBLC scam imitates the real thing

The fraudulent variant keeps the vocabulary and discards the mechanics. A “third-party bank” will “issue” the SBLC without you opening an account. A “leasing fee” of 6–15% of face value is paid up front. A “non-recourse” structure is promised, meaning you owe nothing back. An MT799 “pre-advice” is presented as if it were the guarantee. The numbers are the tell: genuine SBLC fees from real banks run roughly 0.75% to 3% per annum of face value. Anything above 5%, and certainly anything paid as a large advance, is a statistical marker of a scheme.

It is worth being precise about why this can never work as advertised, because the explanation doubles as a detector. Under Basel III, an SBLC is a contingent liability on the issuing bank’s balance sheet. The bank carries the risk until the instrument expires. No regulated bank takes that risk for someone who is not its vetted, collateralised, counter-indemnified client. The “no-account” promise is therefore not a clever shortcut; it is the precise point at which the story stops describing anything a bank can actually do.

The three ways it ends

- The guarantee never issues. You pay the advance leasing fee, receive a handsome PDF with stamps, and the beneficiary’s bank receives nothing. The broker stops answering.

- The guarantee “issues” from an offshore shell. A “bank” in Comoros, Dominica, Vanuatu, or St. Vincent, license either forged or held by an empty entity. When the beneficiary tries to draw, payment is refused or the issuer is insolvent. You owe the supplier and the broker at once, and litigating from the UAE is effectively impossible.

- The document is an outright forgery with a fabricated SWIFT code, used once for a specific deal. The next chapter is a criminal file, and it is on your side of the table.

The regulators have said this out loud

This is not a matter of opinion among trade-finance practitioners. National regulators have published their positions in plain language.

- The FBI, through its IC3 Public Service Announcement of 18 March 2019, documented schemes built on fabricated SBLCs and counterfeit MT760/MT799 messages.

- The U.S. Securities and Exchange Commission’s investor alert, Prime Bank Investments Are Scams, states the regulator’s flat position: “Prime Bank” and “high-yield SBLC” programmes are fraudulent by definition.

- The International Chamber of Commerce, in its guidance through ICC Academy, is explicit that SBLCs are not borrowing mechanisms and cannot be “leased,” “monetised,” or “traded.”

The red-flag checklist

Any single item below is, in practice, sufficient reason to walk away.

- Issuance promised without opening an account at the issuing bank.

- Advance “leasing fee,” “issuance fee,” or “SWIFT fee” above 3% of face value.

- Promise of a “non-recourse” structure where you owe the bank nothing.

- Talk of “monetising” the SBLC into a high-yield programme.

- Issuing bank in an offshore jurisdiction (Comoros, Dominica, Vanuatu, St. Vincent, Marshall Islands).

- An MT799 presented as proof of issuance (it is an advisory note, not a guarantee).

- Issuance promised in 3–10 days (real underwriting takes 4–6 weeks).

- A non-disclosure agreement that forbids discussing the deal with your own bank or lawyer.

- Urgency: “sign today or the slot is gone.”

- Payment requested to an individual’s account, in cryptocurrency, or through a third jurisdiction.

What to use instead

For importing gold from Africa into the UAE, the working instruments are well established and boring, which is exactly what you want.

- A documentary letter of credit under UCP 600, confirmed by a major international bank. This is the backbone of cross-border commodity trade. A genuine UAE trading licence (for example, a DMCC or mainland DED licence) gives direct access to the trade-finance desks of Emirates NBD, FAB, Mashreq, and ADCB. That is the first door to knock on.

- A genuine third-party collateral guarantee, the honest cousin of what the scam imitates. An outside investor posts collateral at the issuing bank itself; the bank issues the guarantee to your supplier; you post a margin of 10–30% and sign a counter-indemnity. Timeline 4–6 weeks, total cost 2–8% of face value, minimum ticket usually from $2M. The decisive test: collateral and issuance happen at the same regulated bank. When they don’t, you are looking at the fraudulent variant.

- Escrow-based structures through DMCC-accredited intermediaries, a workable alternative for deals up to roughly $5M, particularly with new suppliers from Ghana, Mali, the DRC, or South Africa.

The first twist: who is the beneficiary?

Early in the exchange, an important detail surfaced. Meridian was not the applicant, they were the beneficiary. They were the buyer; the supplier was asking for an SBLC in Meridian’s favour to secure payment, with the actual cash for the goods to move separately by MT103 wire after inspection.

This matters, because an SBLC in the buyer’s favour is a standard and legitimate structure. It changes the analysis, but as it turned out, not the conclusion. The legitimacy of the shape of a deal says nothing about the legitimacy of the participants in it. The same red flags apply; they simply view from the other side of the table.

The second twist: the “fund,” and a real bank as set dressing

Pressed for specifics, the structure resolved into something more elaborate. A third party, described only as “a fund”, would act as applicant, blocking its own funds to guarantee the supplier on the buyer’s behalf, in exchange for a fee. An intermediary “arranged” it, for another fee. And the issuing bank was named: IDB Bank, New York.

Here is the point the whole case turns on. IDB Bank is real. It is the Israel Discount Bank of New York, a commercial bank headquartered in the Grace Building at 1114 Avenue of the Americas in Manhattan, chartered by the State of New York, FDIC member, a subsidiary of Tel Aviv’s Israel Discount Bank, with roughly $12.95 billion in assets and ratings of BBB+ from Standard & Poor’s and A− from KBRA. Its head-office BIC in the SWIFT network is IDBYUS33.

And that is precisely the trap. A real, reputable bank in the chain does not validate the other participants. It disguises them. The single most effective ingredient in a convincing fraud is one genuine element around which the rest of the decoration is built. The presence of IDB Bank is reassuring in exactly the way it is designed to be.

The documented cases that match the script

The United States Department of Justice has prosecuted a series of intermediaries who sold versions of this structure. These are public press releases; the dates and outcomes below were verified directly against the DOJ website.

United States v. Douglas, Mignott, Gillar (D.N.J., 24 October 2022)

Three men were convicted by a federal jury of wire fraud. Their company offered to “acquire and provide” an SBLC supposedly backed by either €1 billion in cash or “highly lucrative Mexican gold bonds.” The victim company wanted the SBLC so it could purchase raw gold overseas and sell it to refineries, and agreed to pay $1 million as a “bank fee.” After the victims transmitted $800,000, no SBLC, and nothing of value, ever materialised. The overlap with the structure described to Meridian runs to the level of phrasing: buying gold overseas to resell, an intermediary, an SBLC “arranged” through a third party.

United States v. Markowitz & Binet (S.D.N.Y., 6 March 2020)

Two men pleaded guilty to an advance-fee SBLC scheme that ran from 2012 through 2019. Victims paid six-figure advance fees for SBLCs that were never issued or were fakes. The context was financing for international projects, including oil and gas in Africa. One defendant used fake financial institutions incorporated in Switzerland to lend a veneer of legitimacy. The prosecutors’ own framing is worth reading literally:

“Fraudulent SBLCs are frequently used in advance-fee schemes so that victims provide funds up front in exchange for the promise of an SBLC. In reality, the victim never receives the SBLC or receives a fake SBLC.”

United States v. Hampton, Kuzma, Davis (D.N.J., 1 June 2022)

Three men were charged by indictment in a $3.25 million SBLC “investment” scheme. This one is an indictment, not a conviction, the presumption of innocence applies. The structure, however, is the familiar one: SBLCs marketed as an investment, money wired to an “asset manager’s” account, funds then dispersed.

None of this proves what is happening in any one new deal. But when a fresh proposal lands inside the exact template that prosecutors keep pursuing, that is reason enough not to move without verification. For a broader look at how these schemes fit into the wider landscape of SBLC and bank guarantee fraud, see the companion article on this site.

The economics don’t close

Beyond the pattern-matching, the specific numbers in the offer contained internal contradictions worth spelling out, because arithmetic is harder to fake than paperwork.

The 3–4% fee. If it is an annual rate and the SBLC lives 4–6 weeks, the “fund” earns roughly 0.5% for the month, less than the yield on U.S. Treasury bills. No investor blocks capital below the risk-free rate. If instead it is a one-time fee for the short term, then annualised it is 30–50%, which is implausibly high for a supposedly low-risk operation that merely blocks funds at a bank of IDB’s calibre. And if the fund genuinely bears real risk, that the supplier defaults, the SBLC is drawn, the collateral is lost, then it must hedge that risk through you. Somewhere in the structure a counter-payment or counter-collateral from the buyer must appear. The right question to the intermediary is blunt: how exactly is the fund protected against the buyer’s non-performance and against the SBLC being drawn? If the answer is “it isn’t,” or “an insurer covers them,” the economics stop closing.

The anonymous fund. In a real deal you must know the applicant counterparty’s legal name, jurisdiction, registration number, and beneficial owners, your UAE bank needs it for the later MT103, your lawyer needs it, your own compliance needs it. An intermediary who won’t name the fund before documents are signed or money moves is, by itself, sufficient reason to pause. In genuine trade finance, names are disclosed at the KYC stage.

The supplier’s strange preference. An African gold exporter with real metal and a real bank will usually accept a documentary letter of credit from the buyer’s UAE bank. If a supplier insists instead on an SBLC routed through an outside structure, experience points to one of three things: the supplier is part of the same scheme and earns on the fees; the supplier cannot obtain an LC because it or its bank fails basic compliance, which is itself a bad sign in the gold trade; or the supplier is being defrauded by the same intermediary and the metal may not exist at all.

The verification sequence

The reassuring part of this whole subject is that the entire question is answerable with public tools and ordinary banking procedure, before a single dollar moves.

- Demand the fund’s full identity in writing: name, country of registration, number, beneficial owners. Refusal or evasion ends the conversation. If named, check it against the country’s registry, against sanctions databases, and against public fraud cases.

- Get the responsible banker at the issuing bank from an official source, not the intermediary. Call the trade-finance desk and ask whether the named fund is a client and whether an SBLC with these parameters is being prepared. If the fund is not their client, there is no SBLC.

- Have your own UAE bank send a formal bank-to-bank query to the correspondent at the issuing bank. In trade finance this is routine and usually free. Within 24–48 hours you get a “yes, we are preparing this” or a “no, we don’t know it.” That closes most of the question.

- Move no money: not to the intermediary, the fund, or anyone, until a full MT760 reaches the beneficiary’s bank and is independently verified through the correspondent channel. No MT799 pre-advice, no PDF copy, no “swift copy” screenshot opens a payment.

- In parallel, offer the supplier the alternative: a documentary letter of credit from your UAE bank under UCP 600. If the supplier “cannot” accept an LC, treat that as a strong marker.

The broader pattern: gold, Dubai, and trade-based laundering

This case did not appear in a vacuum. The African-gold-into-Dubai corridor is, by the assessment of regulators and researchers, one of the world’s principal channels for trade-based money laundering and sanctions circumvention, gold is liquid, dense in value, and nearly impossible to trace to origin. The instruments that surround it attract a corresponding density of fraud. A new entity with a financial-sounding name, an unverifiable counterparty, and a payment structure built around an outside “fund” sits squarely in the zone where legitimate trade and laundering infrastructure look superficially identical. The verification discipline above is what separates them.

The lesson, compressed

The structure can look entirely workable: a real bank, comprehensible steps, payment only after the instrument is received. That is not evidence of safety; it is how successful imitations are built. They rest on one genuine element, in this case IDB Bank New York, and decorate the rest around it. The documented Justice Department cases share the mechanics of the offer down to “buying gold overseas to resell.” That does not mean any particular party is a fraudster. It means that, without verifying the specific participants, touching money is premature.

None of the analysis here is legal advice, and the consultant who worked through it was not a lawyer, only an experienced reader of infrastructure and open sources applying general logic. The final judgement on any real transaction belongs to a licensed trade-finance lawyer and the buyer’s own bank, both of whom will look at the same picture from their own side. But the cheapest, fastest, and most decisive move in the entire saga costs nothing: ask your bank to send one query to the issuing bank, and wait two days for the answer before you wire anything to anyone.

Note on anonymisation. “Meridian Metals” is a placeholder; identifying details of the enquiring company have been removed. All external facts, the bank, the SWIFT mechanics, the regulator publications, and the Department of Justice cases with their dates and outcomes, are real and were verified against primary sources at the time of writing.

Frequently asked questions

Can you “lease” or “rent” an SBLC from a third party?

No. Under ICC rules (ISP98 and UCP 600), an SBLC must be issued by a bank for its own client, backed by full collateral. There is no legitimate mechanism for “leasing” a bank guarantee. Every regulator that has addressed the question, the FBI, the SEC, the ICC, has stated this in plain language. Any offer to lease an SBLC is, by regulatory definition, either a misrepresentation or a fraud.

What is the real cost of an SBLC?

Legitimate SBLC fees from real banks run approximately 0.75% to 3% per annum of face value, depending on the applicant’s credit profile and the issuing bank’s internal risk assessment. The applicant must also post 100% collateral (cash, securities, or an approved credit line). Any “fee” above 5%, especially if paid upfront before issuance, is a statistical marker of a fraudulent scheme.

Is an MT799 message proof that an SBLC has been issued?

No. An MT799 is a free-format SWIFT message used for informational purposes only. It carries no legal obligation and is not a guarantee. The actual SBLC is transmitted as an MT760 message, bank-to-bank. Fraudsters frequently present MT799 “pre-advice” messages as if they were the instrument itself. Only a full MT760 verified through correspondent banking channels constitutes a valid SBLC.

How can I verify if an SBLC offer is legitimate?

Contact the trade-finance desk of the named issuing bank directly (using the phone number from the bank’s official website, not from the intermediary). Ask whether the named fund or applicant is their client and whether an SBLC with those parameters is being prepared. In parallel, have your own bank send a formal bank-to-bank query. Both steps are free and routine. If the intermediary objects to either verification step, that is itself a red flag.

Need a second opinion on a deal?

If you have received an SBLC or bank guarantee proposal and want an independent assessment of the structure before committing funds, book a consultation. I review trade-finance instruments, verify counterparty claims against public records, and flag structural red flags, before money moves.

Related trade finance guides

- International Trade Payment Methods: a full guide

- Fraudulent schemes involving Letters of Credit

- Partial confirmation of Letters of Credit

- Trade Finance Guide, Part 2

Need a consultation?

If you need professional expertise, book your free 15-minute consultation.